A reader asked us to write about valuing equities using the Discounted Cash Flow method sometime back. It has been long overdued...sorry dude or duddette...we have been busy analysing some stuff of late. Before you read on, we would like to mention that this method entails a lot, a lot and we mean a lot of assumptions and it is highly theorectical. Garbage in- garbage out. Why do you think Research Reports target prices are nearly always way off target? Anyway, its the thought process that counts and not the final target price. Who knows, when thinking through the process..you may actually gain insights on the stock you are researching. So its not useless..this model.

A reader asked us to write about valuing equities using the Discounted Cash Flow method sometime back. It has been long overdued...sorry dude or duddette...we have been busy analysing some stuff of late. Before you read on, we would like to mention that this method entails a lot, a lot and we mean a lot of assumptions and it is highly theorectical. Garbage in- garbage out. Why do you think Research Reports target prices are nearly always way off target? Anyway, its the thought process that counts and not the final target price. Who knows, when thinking through the process..you may actually gain insights on the stock you are researching. So its not useless..this model.There are many forms of DCF analysis and we will be looking at discounting dividends. This is most appropriate for valuing stable companies (for example in a mature industry) and those that have a consistent payout of dividends . (Please note that there are other types such as discounting Operating Free Cash flow or discounting Free Cash flow ).We will be using SingPost as an example. See below for the yearly dividends they give out. We started from year 2006.

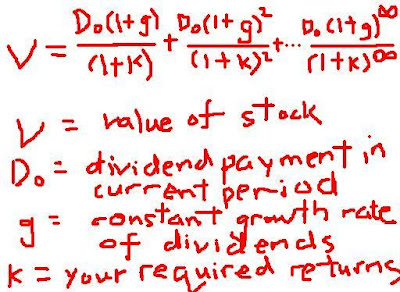

Based on the table above, it is logical to assume that they will be giving out at least S$0.0625 in dividends every year from 2009 and beyond. So here comes the DCF formula. Its looks ugly but its actually quite easy. SGDividends will walk you through.

Based on the table above, it is logical to assume that they will be giving out at least S$0.0625 in dividends every year from 2009 and beyond. So here comes the DCF formula. Its looks ugly but its actually quite easy. SGDividends will walk you through.

Figure 1

Figure 1

As SGDividends is all about making complicated things even easier than easy. We are going to derive a formula which will be easier than easy to use. The derivation is below in figure 2, but you can skip this part amd jump to the final formula in Figure 3.

Figure 2

Figure 2

So let's put all this mumbo-jumbo in practice, shall we?

Let's assume your required rate of return, K = 6% ( We use 6% just to follow the rate from DBS preferential shares. It can be anything you wish because its YOUR required rate of return.Most people would then choose as high a rate of return as possible as more is better right?Then its wrong. You should consider your required rate of return as the rate of return of the next best investment which you think you can get. So if you thought DBS preference shares at 6% is one of the best around or it makes you happy, then use it as a benchmark to input the K.)

Price currently as of 21 Nov 2008 as listed on SGX = $0.76.

No comments:

Post a Comment